GLOBAL ECONOMICS

GLOBAL ECONOMICS COMMENTARIES

Patrick Grady

Flawed Study Implausibly Claims that an Independent Quebec Would Have a Better Credit Rating

June 22, 2026

Last week I got a call from the producer of the Montreal Now Show with Aaron Rand on WJAD asking me to do an interview on study done by Antoine Rondeau for the L'Institut de recherche sur l'autodétermination des peuples et les indépendances nationales. I never cease to be amazed at the extent to which sovereigntists will go to try to make separation from Canada out as costless for Quebec or worse, even economically beneficial as claimed by this study. As the great Yogi Berra once said, "It's deja vu all over again."

In considering this study, you need to be aware that the IRAI is not an unbiased politically neutral economic research institute. It was founded in 2016 by Pierre Karl Péladeau, the former head of the separatist Parti Québécois. And, since its origins it has been presided over by law professor Daniel Turp, who was formerly a Bloc Québécois Member of Parliament, and a Parti Québécois Member of the National Assembly of Québec. The objective of the IRAI is clearly to promote sovereignty for Quebec and that is exactly what this study is attmpting to do.

The study's conclusion that Quebec would actually have a higher credit rating and lower borrowing costs if it were to separate from Canada is preposterous.

Complex econometric models like that built by Antoine Rondeau in this study cannot take into account is the impact of the great uncertainty over currency, debt and trade that is likely to be caused by any major break in economic relations such as would occur if a region were to separate a become an independent country. In Quebec's case, its fiscal position would also be adversely affected by the loss of support from equalization, the Canadian Federal Government Program that shares the revenue that it receives across the country so that all "provincial governments have sufficient revenues to provide their residents with reasonably comparable levels of public services at reasonably comparable levels of taxation." Remember that the lower income provinces like Quebec are the main beneficiaries of this program, which is designed to counter regional disparities.

Rondeau's methodology provides a good example of how complicated statistical analysis, which can only be understood by econometricians, can be used to pull the wool over peoples' eyes. More specifically, Rondeau develops an ordered logit model, using data for over 30 countries from the IMF World Economic Database (and the World Governance Index from the World Bank), which he estimates using an ordered credit rating dependent variable and nine independent determining variables, including:

- the current account balance,

- the structural balance of the government,

- the rate of unemployment,

- GDP growth,

- the share of world GDP,

- real GDP per capita,

- inflation,

- net government debt, and

- the quality of government index.

The model is used to predict the ranking categories that the various countries' credit rating will fall into based on the determining variables. And then presto chango the value of the nine variables calculated for Quebec are substituted into the model as if Quebec were another independent nation to predict what its credit rating would be under the counterfactual assumption that it was an independent country rather than a province of Canada.

An obvious problem with the methodology is that 24 of the 35 countries included in the statistical analysis are members of the EU and except for one all use the euro. Since EU membership is not an explicit variable included variable in Rondeau's analysis, this means that when he puts the Quebec data in the model, he is implicitly assuming that it will get much of the benefit in credit rating that the members in the euro zone enjoy from being an integral part of that larger economic entity. There are, of course, many other problems with this methodology that make its result suspect. Indeed ven for estimating changes in the credit rating of some of the countries included in the database, where its use is more appropriate, it falls short because some of the variables have the wrong sign. For example, for at least some of the countries, the credit rating improves if inflation up or GDP growth, GDP per capita, or the current account balance goes down. But at least for the budgetary balance and government net debt, which are key variables, it has the right directional impact. An additional issue that must be addressed to make an estimate is what is the fixed impact (constant term) in the logit regressions. This is important as it captures the overall positive or negative overall views of the rating agencies about each country.

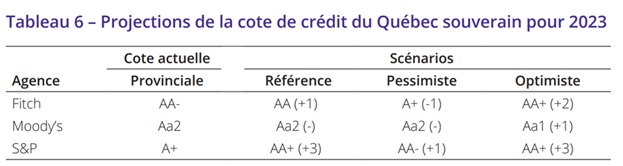

None of these econometric problems deter Rondeau from using his model to estimate the impact of separation on Quebec's credit rating. With respect to the constant term, he makes the heroic assumption that it will be the same as for Canada, a much larger economic unit with its own currency that belongs to the CUSMA. To provide additional alternate scenarios, he goes even further out on the limb and uses the constant term from the regressions of New Zealand and Sweden, based on the justification that they are around the same size as Quebec. He dubs the Canadian case, the reference scenario, the New Zealand case the pessimistic scenario, and the Austrian case the optimistic scenario. His results are shown in the following table, which are cut and pasted from page 13 of his study.

In the reference scenario, Quebec's credit rating as an independent state is projected to go up one level from AA- to AA based on the Fitch rating, stay the same at Aa2 based on Moody's, and go up three levels from A+ to AA+ based on S&P. In the pessimistic scenario based on New Zealand, the credit rating is projected to go down one level based on Fitch and up one based on S&P. But in the optimistic scenario based on EU member Austria, the rating is projected to go up based on all three rating agencies. This is, of course, all pure Fantasyland.

Back in the real world, a point worth bearing in mind is that the United Kingdom, which is an already established and respected world financial center, lost its triple A credit rating as a result of leaving the European Union and to this day has not gotten it back. Brexit was a much smaller shock in relative terms than Quebec separation would be because the UK already had its own currency, the pound, and its own central bank, the Bank of England, to manage the financial fallout of leaving the European Union and cushion the shock. Quebec as a new country emerging on the world stage would be subject to a much greater degree of uncertainty and would have no comparable shock absorbers to cushion the blow.